November 2019 was the point I came out of my very good work pension, with the aim of investing to beat the gains that it could offer.

My work based pension scheme is a mixture of a Final Salary and an Average Salary pension Scheme. Up until 2015 it was Final Salary. Since then it has been Average Salary. They are very good as pensions go. Each additional year of membership will give me approximately £150 income per month at the point that I can draw the pensions, 60 for the old pension and 67 for the new one.

So my investing has a primary goal of earning me £150 per month for each year of investing. 2 years in I should be gaining at least £300 per month of income.

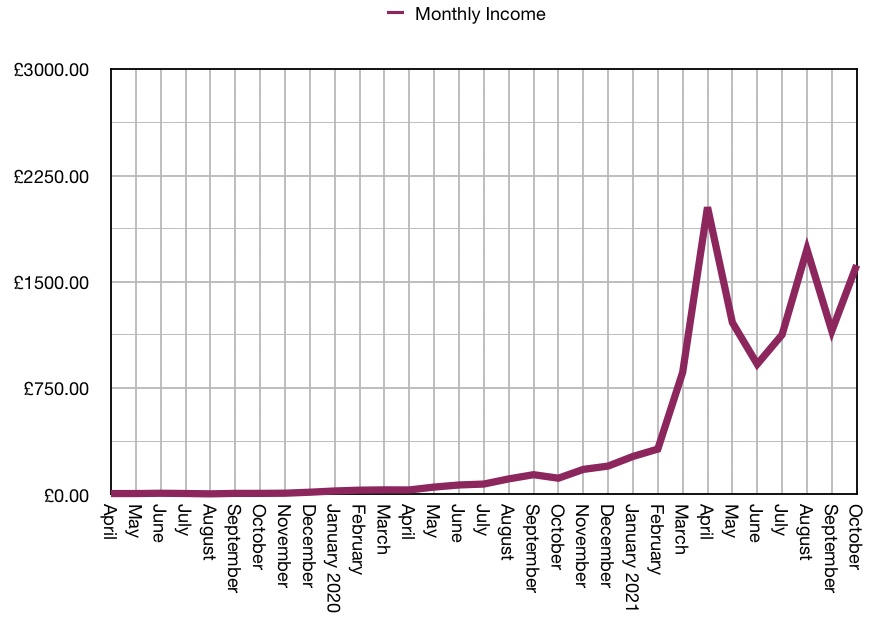

Looking at the graph it is blindingly obvious that I am beating my pension.

Am I an investment Guru?

I think the answer is fairly obviously NO!

I know a little bit about investments and how they work. I have learnt a lot more over the last 2 years and I am certainly better informed now than then.

Did I get lucky?

In some ways the answer is yes. The timing of the crypto bull run has made a significant impact on my wealth creation.

Are my current income streams sustainable?

No is the simple answer. I have some capital in long term traditional and safe investments. But not that much. I am maxing out my ISA allowance each year, which I will continue to do.

The rest of my investments are in highly speculative and higher risk investments. As these markets mature they might become less high risk by default. Alternatively I will need to rotate out of these into lower risk stable investments.

How did I get to my current position?

Not being an investment guru I have done a scatter-gun approach. I have invested an an enormous number of investments and got a feel for their risk and reward profile. Being happy with higher risk has resulted in a few failures. But each time I become a little wiser

I have systematically got rid of investments with a risk/reward profile I didn’t like. On the flip side I have continued to be interested in new opportunities that present themselves.

Things for the Bin and things to keep

Each sector that I have invested in has some merit, but sometimes only 1 or 2 platforms are worth staying in.

The Sun Exchange. This is not going to be as high a reward as I hoped. What I like though is the business model and the team. They have created an excellent product that feels safe. For this reason I will continue to add new funds in the next year. I will reassess on a regular basis. The investments are incredibly illiquid, so they are effectively locked.

Fractionalised property ownership. Although this can be put in an ISA in the UK or earned via crypto abroad, the returns are really modest at 3-5% per annum. The real value comes from sale of the properties 5-10 years down the line assuming a rise in prices. For me 5-10 year time horizons for an unknown gain is not a good fit so I have exited this sector

Crowd funded property development loans. This is a good sector with the right due diligence and a steady supply of investments. Only one platform fits this criterion in the UK. So I have stayed in CrowdProperty but I have exited all the other UK property development loan platforms. In the Euro zone the stand-out performer is Estate Guru, but the increased % return is offset by having to pay tax on the income. As I am trying to minimise the complexity of tax liabilities I will be exiting Euro crowd lending on property development.

UK P2P lending. The only platform worth considering outside of property development loans is ElfinMarket. It’s a great business and wrapped in an ISA. They have very strict lending criteria which makes the investment fairly safe, with acceptable returns. I’ll be staying in this one long term hopefully.

European P2P lending. This sector was very interesting, but over the last 2 years I have seen a number of platforms cease trading with resultant loss of funds for the investors. Compliance and regulation is a mine field. There seems to be a lot of bad actors in the sector. The rewards are good but the risk seems high. For this reason I am exiting most of this sector. I am not yet fully decided about leaving 1 platform with funds. If so, which one?

World wide P2P lending. I have looked at a variety of P2P lending platforms. EthicHub (coffee farmer loans) has a lot of potential but the method of funding is really difficult. For this reason this is on hold for now until they get it sorted. There are also a number of solar power companies to lend to but I am yet to invest with any of them.

Stocks and Shares. This is a complex one. On the one hand this should be a large proportion of my assets. On the other hand it needs to not be a full time job. I started with building up a massive portfolio of individual stocks, both dividend payers and growth stocks. This became a big user of my time. I also wasn’t utilising my ISA facility for this investment. I have moved almost all my funds into an ISA wrapper now and also rationalised my stocks. I now have a dividend heavy portfolio giving me a regular income. I also hold a few ETFs for long term growth and might hold a few individual stocks in the future. It has become much more manageable.

Crypto Lending. As with my other sectors this is full of options, but not all of them are low risk. It’s a young industry and regulation is slow to be implemented. I think I have worked out who the big players are going to be and have already rationalised down to 2 main platforms. NEXO and Celsius are my current winners. All the others have gone.

Yield Farming and DeFi. This was a complete revelation to me. DeFi is where my main interest now lies. It is incredibly early in its development. I will continue to watch, learn and dabble in this space. As the current crypto bull run comes to an end I will transfer a significant proportion of my crypto assets to the Anchor protocol. On Anchor I will be able to earn safe steady yield on the UST stable-coin.

Juicy Fields. This is probably my most speculative play that I will stay in. On the surface it looks like a business model that should work. There are some red flags and so I have limited my exposure. No further new investments, and after I have removed my initial capital in 6 months, it will all be fun money, so no dramas.

Goals for the coming year

November for the last 3 years has yielded £8, £176 and £1430 as a monthly income. There is going to be some serious consolidation this year, so I’m not expecting the same sort of gains.

I would like my passive income to be comfortably above £2000 every month. Hopefully approaching £3000 on occasion.

I would also like to see my passive income supporting my lifestyle, so that I can reduce my hours at work and take home a smaller wage.

Almost forgot… I’m going to take a serious deep dive into the decentralised Metaverse!

Here’s to the next year of investing