Inspiration

I’ve been with NEXO almost since the beginning of their journey in 2018. They launched during the ICO craze of 2017-18. At the start they had a very simple business model. Deposit crypto and earn interest or take out a loan collateralised by your crypto deposits. It was a very simple lending platform. I initially bought their token as it gave a profit share of the business, but soon was sold on the basic premise of the platform and started depositing crypto to earn interest. Since then they have gone from strength to strength.

The blurb from the platform…

Nexo is the world’s largest and most trusted lending institution in the digital finance industry.

Since 2018 Nexo has strived to bring professional financial services to the world of digital assets. Leveraging the best of the team’s years of experience in FinTech along with the power of blockchain technology, Nexo empowers millions of people to harness the value behind their crypto assets, shaping a new, better financial system.

Nexo currently manages assets for 4М+ users across 200 jurisdictions.

Blah, blah, blah… fairly standard stuff.

How does it work?

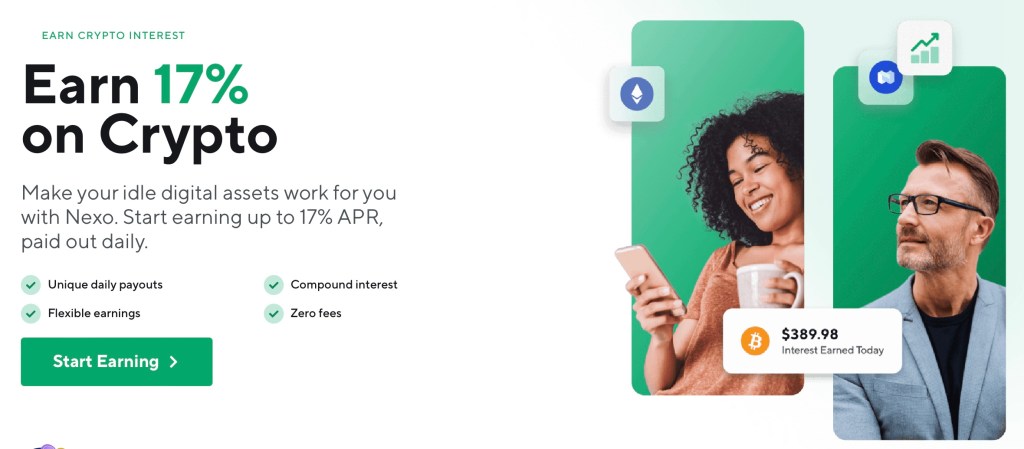

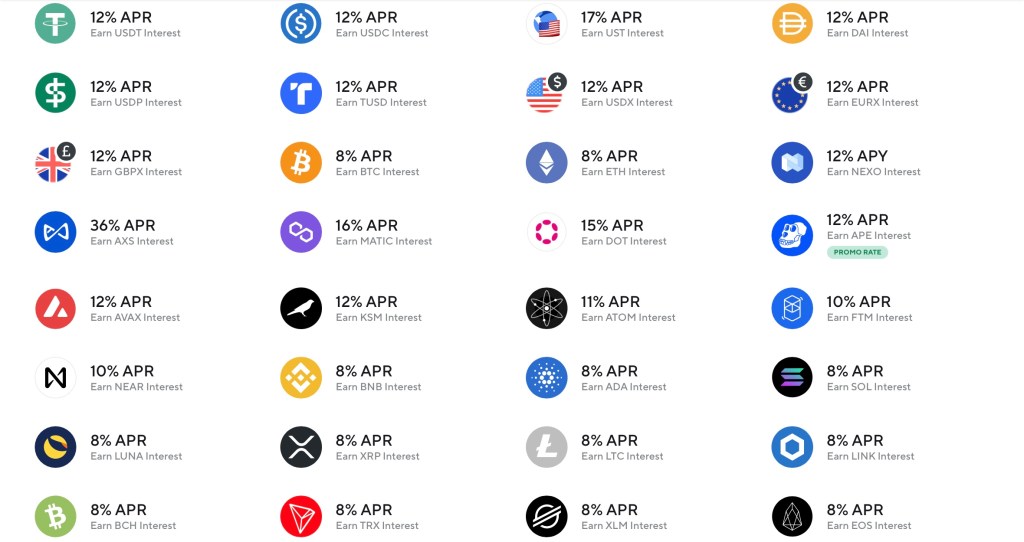

Earn

The Earn product is for me the most important. Simply deposit crypto assets and you start earning daily interest. If you lock up the funds then you can earn higher rates. If you also hold NEXO tokens then you can earn higher rates again.

Borrow

The Borrow product is how NEXO earns their income. They offer very attractive rates depending on your holding of NEXO tokens. Most of their income however comes from lending to Institutional size partners. As a retail borrower your loan needs to be over-collateralised by crypto assets. You then can take your loan as a stable coin or fiat money in your bank account, which arrives almost instantly

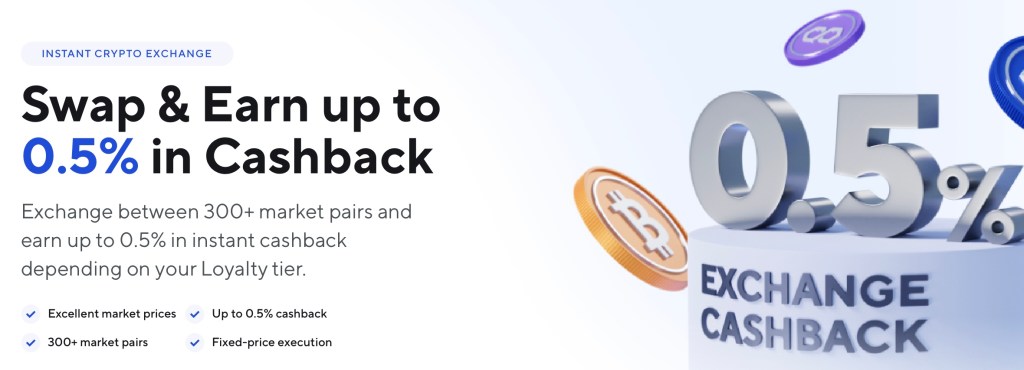

Exchange

They have an in-house exchange where you can exchange your crypto assets and also gain 0.5% cash back. The rates are close to market value but there is a small spread which acts as another income stream for NEXO the business. It’s quick, simple and convenient to use.

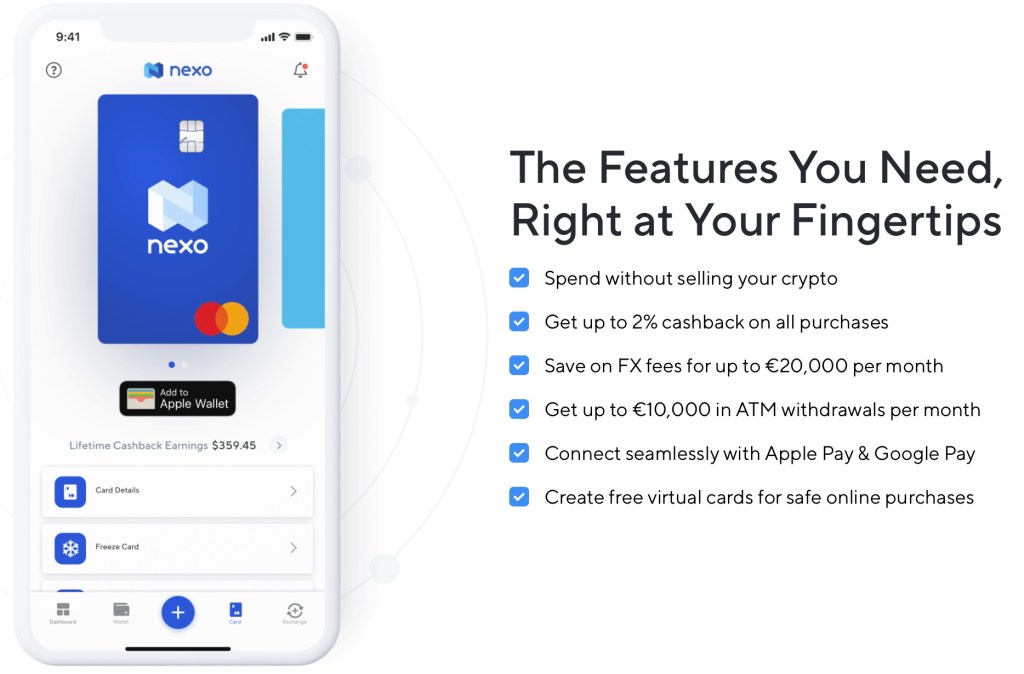

Card

The Mastercard backed Debit Card allows you to spend crypto in the real world, anywhere that Mastercard is accepted. It took a while to arrive in the UK, but I finally got my hands on a NEXO card in early 2022. When you spend on the card the money gets added to your credit line so is effectively a loan at the rate that your credit line allows. For me that is currently 0% interest as long as I stay below 20% LTV.

Licences and Registrations

They have on their website various financial licences and registrations around the world. 23 states within the USA, Canada, Australia, Switzerland, HongKong and Lithuania (European Union).

My journey with NEXO

I started my journey with NEXO when I bought their NEXO token in 2018. I have increased my holding over the following years and at one point held 17,000 tokens. In the first few years they gave an annual dividend to the token holders paid out in more NEXO tokens. They then changed their tokenomics, stopping the dividends and started giving daily interest on NEXO tokens the same as their other crypto assets. After the token rose to over $1 I sold off 7,000 of my NEXO tokens. Currently I hold 10,000 tokens which earn me daily interest.

My confidence in their business model and their desire to become licensed around the globe, along with their competitive interest rates led me to start using their Earn product. I now hold the majority of my BTC holdings with them and all of my ETH. Both of these earn interest on a daily basis. The platform has become a big player in the space along with CELSIUS.

Referrals

NEXO have a referral system where you both earn $25 in BTC once the person signs up with the link and deposits $100 worth of crypto. Tap the button to sign up.