Inspiration

Peer-to-peer (P2P) and peer-to-business (P2B) are some of my favourite types of investment. Much of my portfolio is made up of various forms of this style of investment. It allows you to join together with other investors to act like a bank.

P2P and P2B can be very high risk and so you have to be very careful in this sector. The first risk comes from the person or business defaulting on the loan. The second risk comes from the platform administrating the loans. They can act fraudulently or collapse if their business model doesn’t work.

I discovered Crowd Property in 2019 and it stood out from its peers for a variety of reasons

- UK based (which is where I am based)

- Authorised and regulated by the Financial Conduct Authority

- Good operating history since 2014

- All loans backed by 1st charge security on the property

- 100% payback (so far)

- Tax free investing via Innovative Finance ISA

- 8% pa earnings

- 2-3 projects launched each week

- Auto-Invest feature to make it hands-off investing.

The blurb from the platform…

“Founded in 2014, we have swiftly become one of the UK’s leading property specialist peer-to-peer lenders, facilitating millions of pounds worth of short term loans to SME property professionals.

CrowdProperty has been FCA authorised and regulated since the 1st November 2017 having proven that our process are robust, our platform stable and our due diligence rigorous, as well as confirming our commitment to transparency and client focus. In September 2018 we became a member of the Peer-to-Peer Finance Association, elected by the biggest and most reputable platforms in the sector for our exemplary operating process. We continue to invest across all levels and functions of the business.”

How does it work?

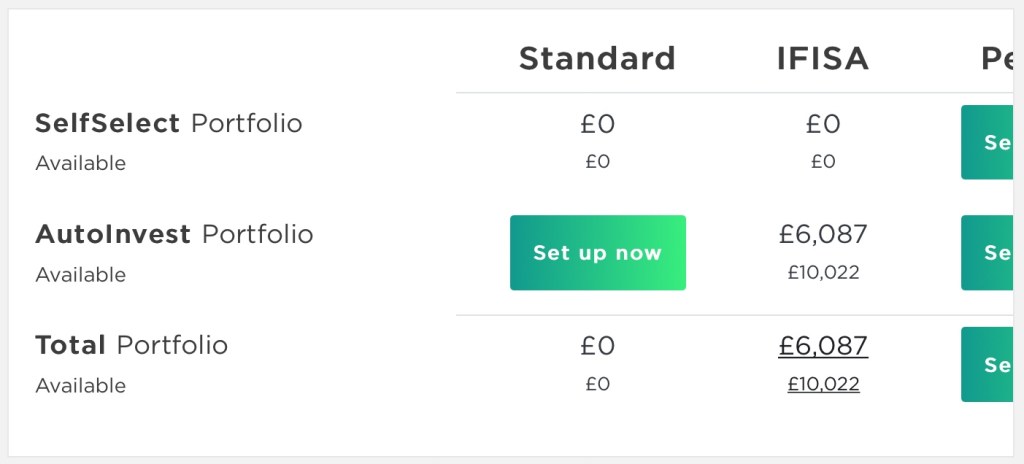

After registering and setting up your profile you will need to deposit money into one of 3 accounts: Standard, IFISA or Pension. Yo will also need to decide if you want to self select your investments or use the auto-invest feature. you can hold investments in all the types of account if you wish.

2-3 times a week a project will go live. CrowdProperty will have done all the due diligence and created an information pack. The information pack is available the day before the project goes live for you to read. You will be emailed the day before to inform you. You will also be emailed on the morning that the project goes live.

At 10am the project will open for funding. Projects are selling out in just a couple of minutes at the moment, so the only way to insure your investment occurs is to use the Auto-Invest feature, unless you have the time to wait by a computer at exactly 10am.

After your funds are pledged, CrowdProperty take care of signing all the contracts with the developer. Once completed the funds are taken from your account and the loan is advanced to the developer. This takes around a week.

Loans are typically at 8% pa. They range from 12-18 month in duration. Most are “full bullet” and so all the interest is paid at the end when the loan is paid back. A proportion of the loans are “bullet” and pay interest at regular intervals, often monthly.

Lots of the developments require funding in phases with new loans launching on the platform after certain milestones have been reached. You can end up being exposed to the same project multiple times, so you need to be aware of this and decided if this fits with your risk profile.

My journey with Crowd Property

I made my first deposit on the platform in November 2019 for the sum of £500. With the aim of my retirement income being as tax free as possible, I started with the IFISA account. Happy that the due diligence by the platform was exceptional, I decided not to spend time researching each project and instead selected the auto-invest option.

Over the next 3 weeks my £500 was deployed over a number of projects. Since then I have made a regular £500 deposit at the start of every month. By November 2020 I had £6,000 deployed on the platform

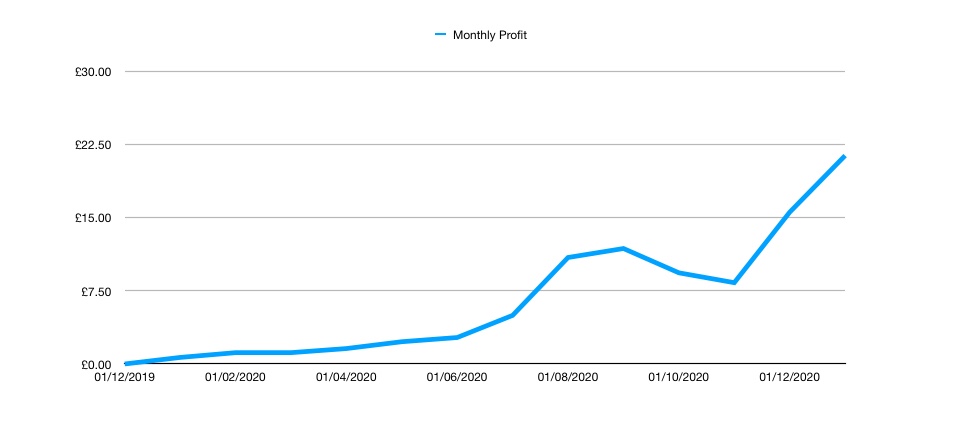

Earnings haven’t been significant yet. With the majority of the projects being ‘full bullet’ and only paying out at the end of the loan term, I am only just starting to see the interest starting to flow from the first projects. Some of the projects have been paying interest monthly so there has been some income, which is slowly increasing. See chart

I am extremely happy with the way CrowdProperty has coped with the Covid situation and how well it has communicated regarding any delays to projects. It looks to be a business going from strength to strength. I am very comfortable with my money being invested here. In line with my plan towards the end of 2020 to make larger investments less frequently, I decided in November to deposit £10,000 on the platform. It will take a while to deploy all the money as often a pledge in any project is only £50, but over the coming months it should get deployed.

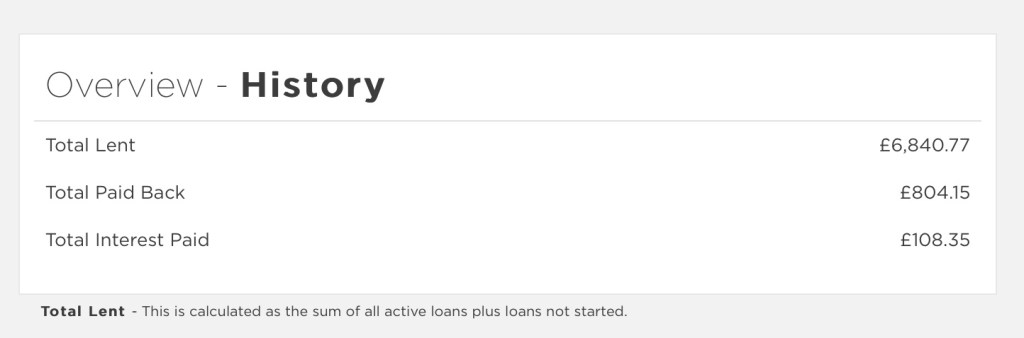

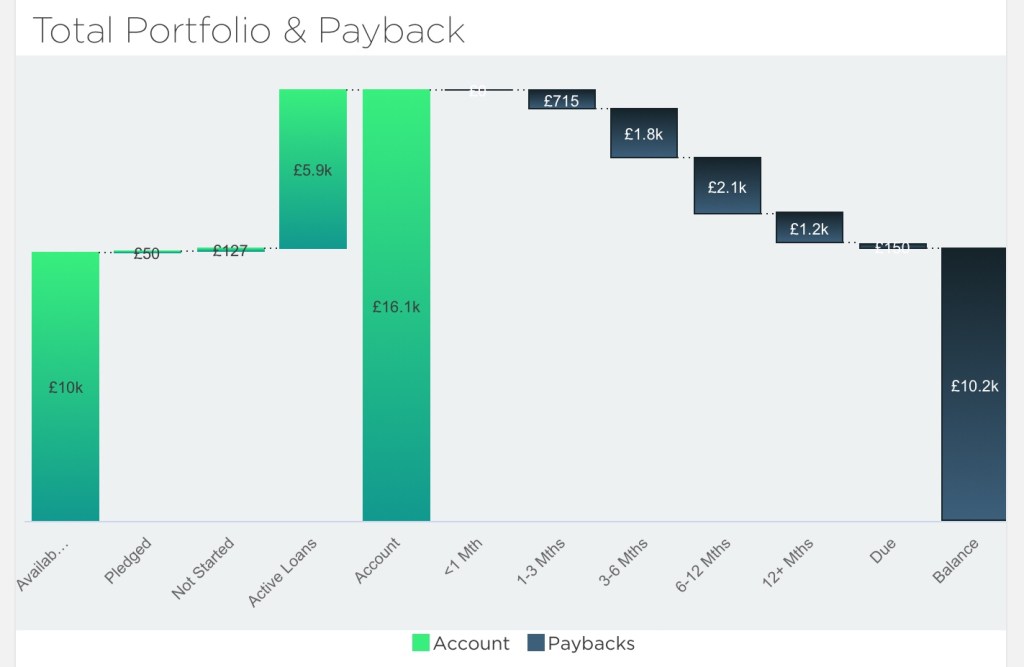

The Website gives lots of metrics so you can track your investments. Below is the totals for all my loans so far. As you can see, interest paid as a proportion of total lent is very small, but most of the loans are still active. Interest as a proportion of total paid back is very healthy. Overall as time passes, I’m expecting the 8% predicted in the blurb.

At the time of writing (January 2021) this is what my portfolio looks like…

Own a part of the business.

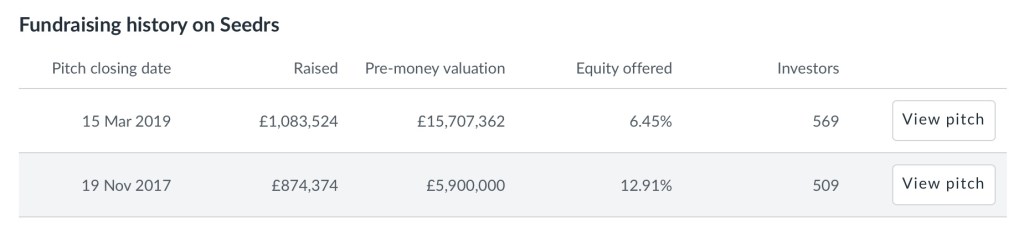

CrowdProperty has had 2 equity crowdfunding rounds on Seedrs

I wasn’t aware of the company at the time of the equity raises either in 2017 or 2019. But as Seedrs has a secondary market, I have managed to purchase a small number of shares (6). I believe not only in using the platform but it seems to be a very successful business model as well. One worth owning equity in.